Most of us were raised to believe that hard work is the key to financial success.

Work more.

Work longer.

Work harder.

But if hard work alone built wealth,

every nurse, every teacher, every essential worker, every single parent, every immigrant hustling day and night would be financially free.

Yet most aren’t.

A 2024 Paycheck-to-Paycheck Report from ACA International found that 65% of consumers currently live paycheck to paycheck, meaning a missed or delayed paycheck could cause serious financial difficulty. acainternational.org

And that’s not because people are lazy or irresponsible.

It’s because they’re trapped in a system that rewards effort — but not ownership.

As a nurse, I saw countless patients struggling with high blood pressure, anxiety, and chronic health problems where financial stress wasn’t the only issue—but it was always present in the background. The American Public Health Association notes that unsecured debt is linked to stress, anxiety, depression, and high blood pressure, and that rising household debt threatens public health. American Public Health Association

As a financial educator, I’ve watched hardworking families doing “everything right” — going to work, paying bills, trying to save — and still living with constant money pressure, no margin, and no real plan for the future.

The truth is simple:

Hard work is honorable, but it is not a wealth strategy.

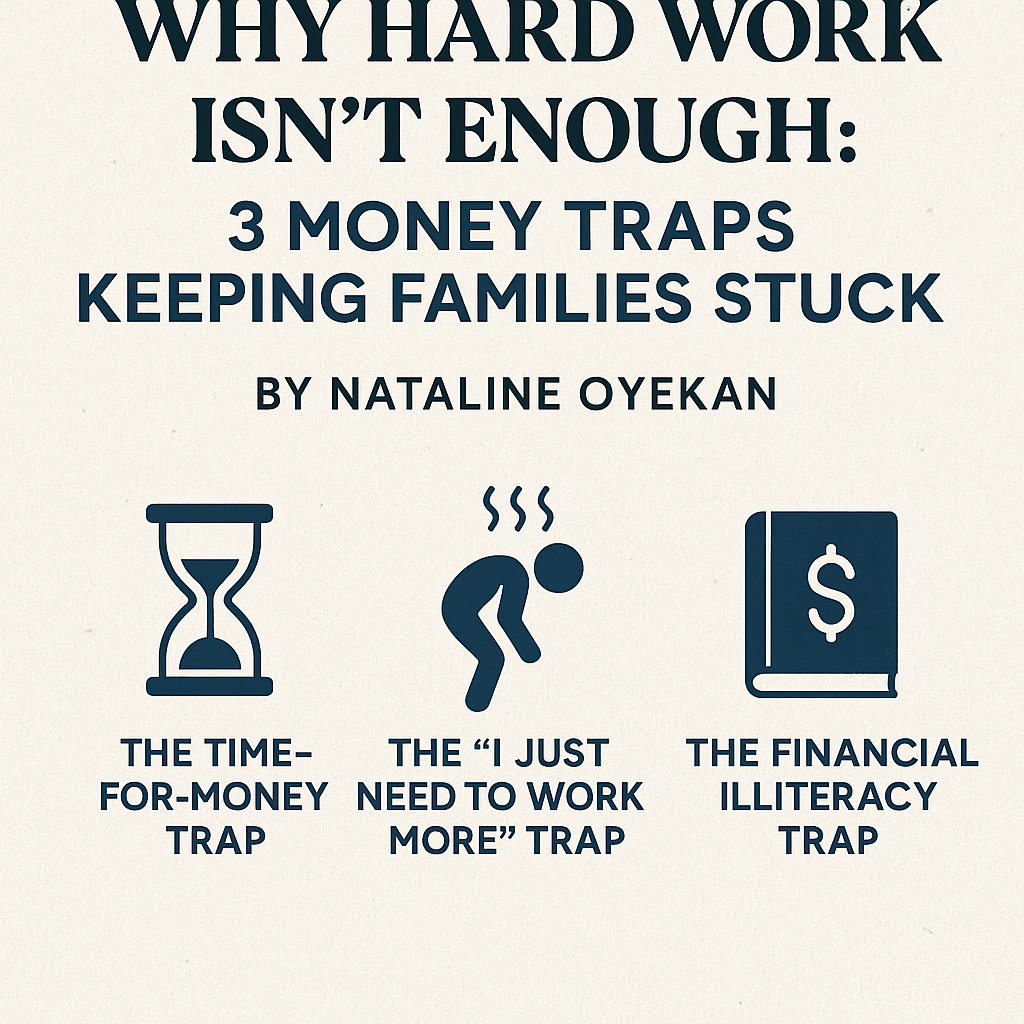

Here are 3 money traps that keep so many families stuck — and what to do instead.

1. The Time-for-Money Trap

This is the biggest trap of them all:

You only get paid when you’re working.

Whether it’s hourly wages or a salary, your income depends on your time — and time is limited.

When time stops — through illness, layoffs, caregiving, or burnout — income often stops too.

This trap creates:

- constant stress

- ongoing fear of what happens if you can’t work

- exhaustion from trying to hold everything together

- limited financial growth, because you’re capped by hours and energy

- dependency on a single source of income

Data shows that millions of people are trying to “patch the gap” by working more than one job. According to analysis based on U.S. Bureau of Labor Statistics data, about 8.4 million people in the U.S. — roughly 5.2% of employed adults — work more than one job. Self+1

Hard workers don’t usually lack discipline or ambition.

They lack leverage.

Leverage is what happens when:

- your money works even when you’re resting

- your skills are packaged into assets (books, businesses, intellectual property)

- your protection strategies (like properly designed insurance, emergency funds, and income streams) keep your family secure even when life happens

Real financial safety doesn’t come from squeezing more hours into the day.

It comes from building structures that protect you when you can’t work.

2. The “I Just Need to Work More” Trap

This trap whispers:

“If I could just work a little more…

If I could just pick up more overtime…

If I could just add one more side job…

then I’d finally be ahead.”

For a season, extra work can help stabilize things. But as a long-term strategy, “just work more” is a recipe for:

- burnout

- strained relationships

- declining physical and mental health

- and still, capped income

Research consistently shows that financial worries are closely tied to mental health. A 2022 study in the journal BMC Public Health found that debt and loans are positively associated with psychological distress, including higher levels of anxiety and depression. PMC A 2022 systematic review in Frontiers in Psychology concluded that financial stress is positively associated with depression across most of the studies reviewed. PMC

Beyond mental health, physical health is also affected. Purdue University has highlighted research showing that individuals with high financial stress are twice as likely to report poor overall health and four times more likely to complain of physical ailments. Purdue University+1

That means your body is paying a price for financial pressure — even when you “push through.”

You cannot build generational wealth by sacrificing your health, your peace, and your relationships to endless work.

You build it through:

- strategy – understanding how money actually works

- systems – automating savings, protection, and investments

- protection – using tools like life insurance with living benefits, emergency funds, and proper planning

- ownership – of assets, not just labor

At NatalineOyekan.com, my goal is to help you move from:

“How can I work more?”

to

“How can I make my money and decisions work smarter for me, my health, and my family?”

3. The Financial Illiteracy Trap

This is the most heartbreaking trap of all — because it’s not our fault.

Most of us were never properly taught how money works.

- Schools didn’t teach it.

- Many parents didn’t know how to teach it.

- Most of us were taught to earn, but not to build, protect, and multiply.

Financial literacy in the U.S. has been measured for years through tools like the TIAA Institute–GFLEC Personal Finance Index (P-Fin Index). The 2025 P-Fin Index shows that U.S. adults, on average, correctly answered only 49% of the financial literacy questions, the same low level as in 2017. TIAA+1

In other words, half of the basic personal finance questions are answered wrong on average — not because people aren’t intelligent, but because they were never properly taught.

A 2025 report on the financial literacy crisis in America notes that only 19% of U.S. adults say they took a personal finance class in high school, and only 29 states currently require a standalone personal finance course as a graduation requirement. Petersen Hastings+1

That means:

- The majority of adults were never taught how to manage money.

- Most were sent into adulthood without a clear roadmap.

So we grow up knowing how to:

- work

- spend

- get degrees

- get jobs

…but not how to:

- grow money

- protect our families from financial crisis

- invest wisely

- build tax-advantaged or tax-free income

- escape destructive debt cycles

- create and transfer generational wealth

Every family deserves access to the knowledge that was denied to them.

Financial literacy isn’t a luxury skill.

It’s a form of healthcare, because money stress is one of today’s most silent killers.

So What Actually Builds Wealth?

If hard work alone isn’t enough, what does move a family from survival to stability—and from stability to freedom?

Here are some of the foundations I teach through my work and here at NatalineOyekan.com:

- ✔ Understanding money systems – learning how banking, interest, debt, taxes, and investments really work

- ✔ Building protection – using tools like life insurance with living benefits, disability protection, and emergency funds so one event doesn’t wipe everything out

- ✔ Creating multiple streams of income – not just more jobs, but different types of income (business, royalties, interest, dividends, etc.)

- ✔ Saving with intention – automated saving, goal-based funds, and strategies that align with your values

- ✔ Using time as a tool, not a trap – letting compound growth work for you instead of delaying planning until it’s “too late”

- ✔ Planning for emergencies – so a crisis doesn’t become a catastrophe

- ✔ Passing down knowledge, not just possessions – teaching children and the next generation the money lessons we didn’t receive

Hard work matters.

Character matters.

Discipline matters.

But they must be paired with the right information and the right strategy.

Why This Matters for Our Families

The cycles we don’t break, our children inherit.

The stress we carry, they feel.

The stories we rewrite, they benefit from.

We do not break generational poverty with hustle alone.

We break it with:

- wisdom

- protection

- ownership

- empowerment

When we learn to see money differently, we also start to feel differently:

- less fear

- more clarity

- less chaos

- more intentionality

And that shift doesn’t just improve bank accounts—

it improves health, relationships, and legacy.

Final Thoughts

If you’ve been working hard but still feel stuck, nothing is “wrong” with you.

You are not failing.

You are trying to win a game where many of the rules were never explained to you.

But once you understand these traps, you are no longer powerless.

You can rebuild.

You can rise.

You can choose differently—

one decision, one habit, one strategy at a time.

Your journey to financial freedom doesn’t begin with a raise.

It begins with awareness, knowledge, and aligned action.

And that’s exactly what I’m committed to sharing with you.

Join the Money Freedom Readers Circle

If this resonated with you, I invite you to stay connected.

At NatalineOyekan.com, I share:

- practical financial insights

- lessons from my journey as a nurse and financial educator

- updates on my upcoming book Salary Is the New Debt

- tools to help you build financial freedom without sacrificing your health

👉 Get financial insights, book updates, and behind-the-scenes lessons delivered straight to your inbox:

➡️ Subscribe to the Money Freedom Readers Circle at NatalineOyekan.com